By

By

Intro

This article on "California Land Values, What's Going On?" is a new series from Bountiful in collaboration with Terra West Group. In the article Donny covers how farmland prices in California are being impacted due to economic factors, the effects on farmers, access to capital, and why the focus on water.

Summary

Below, we dive into the complexities of the new farmland market landscape. California farmland values have traditionally been attributed to on-farm performance like location, crop characteristics, and ultimately production; all internal to an operation. In recent years, we have seen a shift in farmland values due to more external pressures like elevated input costs, high interest rates, regulations (water availability), and sentiment. These new factors have dampened the market.

However, like in all markets, farms have adapted and shown resilience. Improved efficiencies, slowed acreage growth and strong consumer demand are all contributing toward an upward tick in the market. To navigate the new landscape and continue towards an upward market swing, it's our goal to be your trusted resource helping you stay ahead of the ever-changing market.

When analyzing farmland markets, California is by far the most complex and unique, characterized by its inherent regional differences in farmland values. Due to its substantial variety of crops, regulatory nuances, soil productivities, growing climates, topographies, and water districts, regionalized markets are formed.

The Farm Income Boom. Since 2010, California has experienced a notable upswing in farmland values. The trend can be attributed to favorable commodity prices, especially in tree nuts, and suppressed interest rates, enabling buyers and investors to expand their operations. This financial boost empowered farmers and investors, allowing them to bid on farmland without excessive dependence on debt financing, which ultimately led to artificially inflated asset values.

Has the Tide Turned? Starting in 2020, a cyclical pattern began to emerge in the California ag markets. A paradigm shift in a myriad of economic forces has introduced new variables into the economic landscape not only impacting farmers but also casting a shadow over the once-thriving farmland market.

|

“Over the previous two decades, several macroeconomic measures indicate farmland values have become less correlated with the farm-related characteristics to support their values.” |

Farmland values traditionally have a direct relationship with economics, crop productivity, and property characteristics. Such property characteristics typically include crop type, geographic location, infrastructure, and enabling features such as water resources. However, over the previous two decades, several macroeconomic measures indicate farmland values have become less correlated with the farm-related characteristics to support their values.

Economic pressures have mounted creating this shift in the ag economic landscape translating to a decrease in buyer interest and farmland acquisitions, ultimately contributing to a cooling effect in farmland values.

In this article, we explore the intricate web of factors contributing to this cooling effect in farmland values throughout the Golden State. As the saying goes, "History repeats itself," some are suggesting similarities to the signs observed in the early 1980s. We guide you through a series of events, factors, emerging patterns, and explore potential outcomes during this shift in California's ag economic landscape.

Economic Factors

California agriculture continues to face several challenges that will impact the productivity and economic profitability of the state’s agricultural sector. Let us examine factors affecting the farmland market.

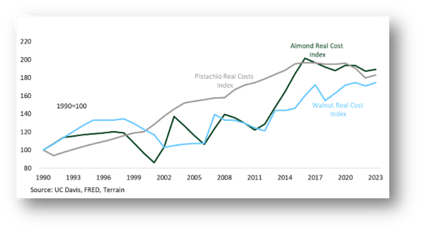

Low Commodity Prices: The saga of diminished commodity prices and outlook, especially tree nuts, has become a cautionary tale for farmers and potential farmland buyers or investors.

Elevated Input Costs: The greatest problem for farm margins heading into 2024 is the elevated cost of production. The impact of higher inflation has been felt, driving farm input costs up, and likely to remain stubbornly high.

Availability of Inputs: Disruptions in the availability of essential inputs such as water resources, chemicals, feed, and labor can create an atmosphere of uncertainty while inflating overall costs in many cases.

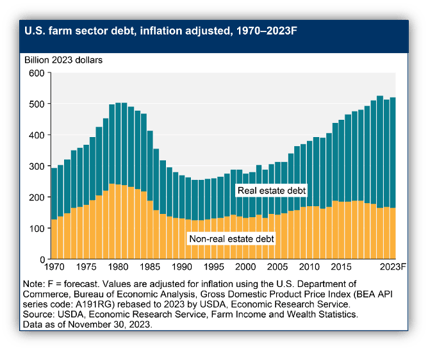

Rising Interest Rates: The persistent rise in interest rates has had a significant impression on operating margins and a direct impact on the cost of capital, affecting the decision-making of producers and investors. According to the USDA’s latest estimates on the U.S. farm economy, interest expense in 2023 was estimated to be 34% higher than in 2022, and 55% higher than in 2021, the highest since 1991, leaving an impact on farm budgets. If the current trends persist, one must wonder how farmers will adjust their crop budgets and debt usage to navigate a world with elevated borrowing costs.

|

“Interest expense in 2023 was estimated to be 34% higher than 2022, 55% higher than 2021, leaving an impact on farm budgets.” |

Regulations: Stringent policies such as water regulations restricting water usage, and environmental regulations aimed at addressing issues like air quality, pesticide use, and labor standards contribute to compliance challenges, adding complexity, costs, and risk to farmland ownership.

Market Dynamics: Ag markets have seen volatility due to factors such as supply chain disruptions, international trade agreements, geopolitics, currency fluctuations, and changes in demands, directly influencing commodity pricing and the state economy. Reduced economic growth typically leads to a reduction in disposal income, which can decrease the demand and pressure output prices. This turbulence contributes to a challenging environment for agricultural commodities, especially almonds, walnuts, and pistachios.

Consumer Preferences: Shifts in consumer preferences towards healthier and more sustainably produced foods have influenced crop choices and production methods. In addition, pressures have been mounting on consumer wallets, resulting in a change in consumer priorities & preferences, as seen recently with tree nuts.

Effects on Farmers

Effects on Farmers

The financial health of farming operations in California can vary depending on several factors, including crop prices, weather conditions, water availability, labor costs, market demand, and cost of capital. As a result of the present state of the California ag economic landscape, let us examine some of the general effects we are seeing on the financial positions of farming operations.

Eroded Operating Margins: The current economic environment has impacted crop sales, primarily due to elevated input costs and low commodity prices. This has contributed to the erosion of operating margins and reduced profitability, ultimately impacting working capital, net worth, and rate of return on farm equity.

Cash Flow Shortfalls: Generally, the operating losses that we are observing indicate a decrease in revenue as well as an increase in operating expenses. When losses persist for extended periods, as we are beginning to see for some operations, challenges can arise when it comes to meeting short and long-term debt obligations due to cash flow constraints.

Weakened Liquidity Positions: Operating losses generally result in a decrease in current assets or an increase in current liabilities, it can impact the working capital of the operations and, consequently, the cash flow. When liquidity and working capital are depleted, producers are left with the choice to seek more credit to replenish their working capital position to accommodate their operating capital needs.

Increased Cost of Capital: The elevated cost of capital and a reduction in the availability of financing raises challenges for some farmers, as interest is beginning to make a greater impression on operating margins, impacting repayment capacity. Like clockwork, sustained inflated interest rates will inevitably slow the expansion of the agriculture sector.

Increased Financial Leverage: Over the past decade, inexpensive debt capital perpetuated a cycle of increased farm debt levels. Higher interest rates in the face of lower net farm income suggest greater use of credit and can pose financial risks from a cash flow standpoint, causing debt to be increasingly harder to service over time.

Declining Farmer Sentiment: A negative outlook among farmers and landowners coupled with the market “narrative” further compounds the challenges, influencing potential buyers to adopt a cautious stance and avoid entering the market or expanding operations.

Lending Environment

Lending Environment

As uncertainties in the agricultural sector prompt lenders to exercise caution and reassess their exposure, the repercussions are creating lending constraints in today's market, influencing credit quality concerns, shifting lending concentrations, necessitating adjustments in lending strategies, and contributing to changes in lending activity across the industry.

|

“Over the past decade, inexpensive debt capital perpetuated a cycle of increased farm debt levels. Higher interest rates in the face of lower net farm income suggests greater use of credit and can pose financial risks from a cash flow standpoint, causing debt to be increasingly harder to service over time.” |

Credit Quality Concerns: Lenders are beginning to sense signs of weakness and distress in specific commodity sectors. As a result, more caution is being taken when considering extending credit for ag operations, potentially limiting their lending activity and creating a hurdle for those seeking financing. This can potentially cause a ripple effect resulting in a more challenging environment for agricultural stakeholders to access the necessary financial resources, potentially hindering growth and sustainability in the sector.

Lending Concentrations: We are beginning to see certain concentrations of lending in specific commodity sectors, prompting lenders to reassess their exposure and decrease their willingness to extend credit.

Lending Concentrations: We are beginning to see certain concentrations of lending in specific commodity sectors, prompting lenders to reassess their exposure and decrease their willingness to extend credit.

Adjusted Lending Strategies: The evolving economic conditions of today are leading to adjustments in lending strategies, resulting in less favorable terms for farmers and buyers seeking financing.

Changes in Lending Activity: Entering into the 2024 crop year as interest rates remain steadily high while commodity prices remain less than desirable, we are seeing a decrease in farm lending activity for real estate acquisition financing. Meanwhile, a pattern has emerged showing a rise in operating and restructuring loan activity as a result of financial weakness at the farm level.

The Focus on Water

The Focus on Water

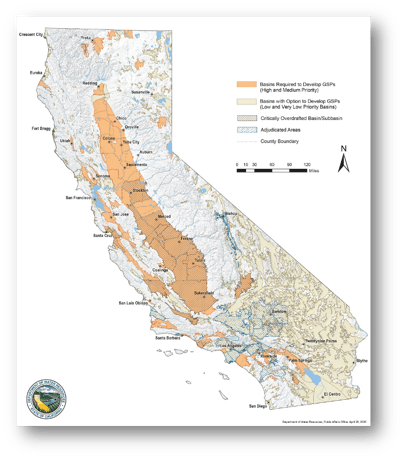

The applications of the Sustainable Groundwater Management Act (SGMA) have raised concerns and imposed threats to farmland production and values in the Central Valley. As these restrictions take effect, farmers face the risk of reduced water availability, potentially jeopardizing crop yields and overall farmland productivity. The implementation of SGMA has led to debates over water allocations and the potential impact on existing water users, sparking uncertainty in the agricultural sector. This uncertainty has created challenges for farmers in planning their long-term operations, as they grapple with the expectation of reduced water availability and the associated economic implications.

Who’s Affected the Most? The proposed impositions hold the potential to significantly rearrange agricultural production and crop selection, especially in the top nut-producing regions. Forecasts predict that substantial tree nut acreage will need to be idled while water diverts to more valuable production areas.

The Effect on Farmland Values: As water becomes increasingly limited and regulated, the economic viability of farming in the region is at risk. This uncertainty has impacted market values of select farmland, as potential buyers and investors factor in the changing dynamics of water availability and the associated risks.

Location, Location, Location: As the inevitable realities of SGMA continue to loom, the differences in individual water districts continue to strengthen their influence on land valuations. Districts with superior surface water entitlements and basins with well-managed groundwater reserves hold the highest regard with buyers and investors while land values in regions reliant upon pumping groundwater continue to soften based on SGMA concerns and implementations.

Final Thoughts

Final Thoughts

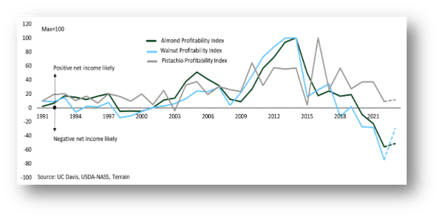

Progressing into 2024, the agricultural landscape in California confronts sustained high interest rates, lower commodity prices, and rising input costs, potentially impacting investor sentiment and farmland valuations. Land values change as the probability of future cash flows changes. Yet, the horizon reveals some positive shifts, notably within the nut sector, where profitability indices are showing signs of improvement. This upward potential is fueled by increasing consumer demand, the slowing growth of acreage, and the lifting of tariffs, which collectively contribute to higher prices than those observed in the last 1-2 years.

|

“Land values change as the probability of future cash flows change.” |

Despite these economic challenges, farmland investments exhibit resilience and maintain their appeal, offering unique advantages such as inflation protection and long-term growth potential. As with any investment, adopting a well-researched, diversified, and patient approach is crucial for navigating the hurdles and reaping the rewards of the agricultural investment landscape. In the end, farmland isn't just an asset; it's a connection to the vital industry that sustains us all.

Ultimately, the dynamics of farmland prices hinge on the fundamental balance of supply and demand. A consistent trend in recent years has been the limited availability of farms for sale in primary farmland markets. The demand for high-quality farms, particularly those with reliable water resources, remains stable.

In California's agricultural real estate sector, the near future presents a landscape that is both dynamic and challenging for some, while also revealing substantial opportunities. As we navigate the complexities of the anticipated 2024 market, it becomes crucial to align with experienced real estate experts who understand the intricacies of this evolving landscape.

We encourage you to reach out to Donny for an in-depth exploration of these insights to stay ahead of the trends and learn how our expertise can steer you toward successful outcomes.

References:

- Tree Nut Profitability Index Chart (Terrain - Low Profitability Likely to Continue for Nut Crops in 2023/2024)

- Tree Nut Real Cost Index Chart (Terrain - Low Profitability Likely to Continue for Nut Crops in 2023/2024)

- US Farm Sector Debt Chart (USDA ERS – Debt, Assets and Wealth)

- Statewide Map of Current SGMA Basin Prioritization (CDWR – Basin Prioritization)

Terra West Group Disclaimer: The information provided in this communication/newsletter is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. Terra West Group does not make any representation or warranty regarding the content and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will Terra West Group be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.